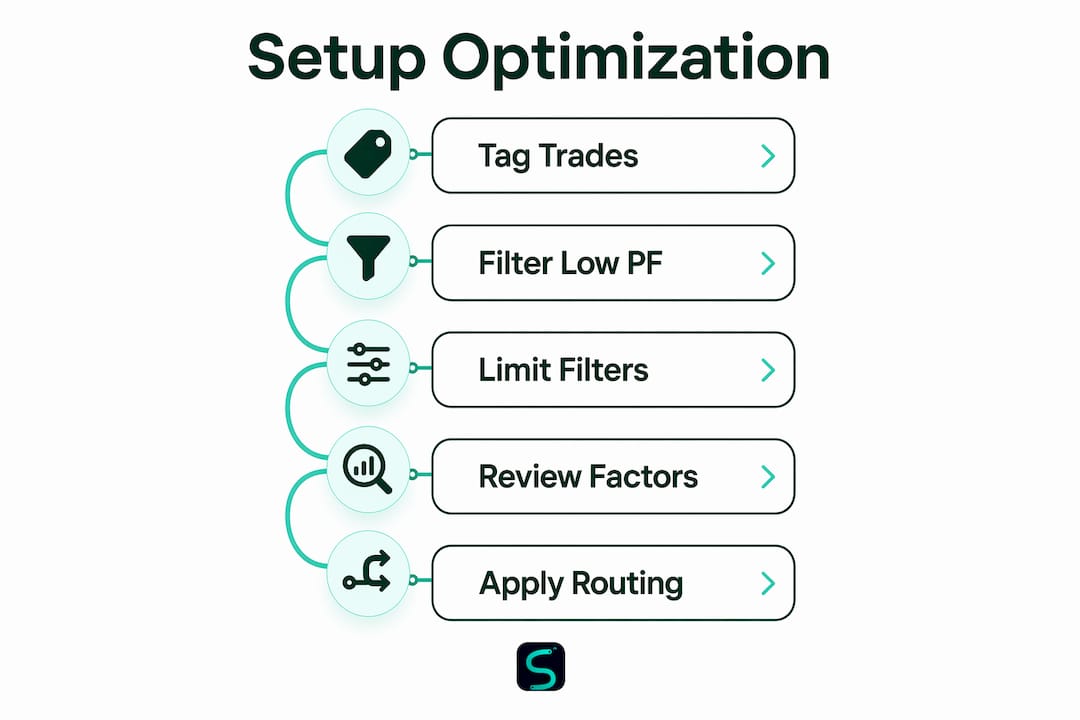

Optimizing trading setups is the process of systematically identifying your highest-performing trade categories and eliminating or adjusting the ones that drain your edge. Most retail traders focus on finding new strategies when the real gains sit inside their existing data. Tag every trade at entry with a setup category and a confidence level, then measure each group by profit factor, win rate, and R-multiple. Tools like trading journals, TradingView, and performance dashboards make this process repeatable. The result is a tighter, data-driven roster of setups that compounds your edge over time rather than diluting it.

How to optimize trading setups by categorizing and filtering performance

The foundation of any trading setup optimization technique is clean, consistent trade tagging. At the moment of entry, assign every trade a setup label (breakout, pullback, reversal, range fade) and a confidence rating (high, medium, low). This takes five seconds and unlocks months of analysis. Without it, you are averaging across setups that behave completely differently, which hides both your best edges and your worst leaks.

Once you have 30 or more tagged trades per category, run the numbers. The three metrics that matter most are profit factor, win rate, and average R-multiple. Profit factor above 1.3 over 30 or more trades signals a meaningful edge, above 1.5 is strong, and above 2.0 is excellent. That benchmark gives you a concrete threshold for deciding which setups to keep and which to cut.

Here is the filtering process in order:

- Export your trade log and group trades by setup label.

- Calculate profit factor for each group. Any group with a profit factor below 1.0 and at least 20 trades is a confirmed loser. Cut it.

- Apply secondary filters such as confidence level or session time. Compare profit factor across subgroups.

- Rank surviving setups by profit factor and R-multiple. Allocate more size to the top two or three.

- Review monthly. Markets shift. A setup that worked in Q1 may underperform in Q3.

Eliminating setups with a profit factor below 1.0 can improve monthly P/L by 30 to 100 percent without changing a single strategy parameter. That is not a marginal gain. It is the difference between a losing month and a profitable one.

Pro Tip: Tag FOMO trades honestly. Trades taken without a defined setup consistently produce worse results, and tagging them accurately is the only way to surface that cost in your data.

What sample size do you need before trusting your data?

Statistical validity is the most overlooked concept in retail trading analysis. Traders routinely make setup decisions based on 8 or 12 trades, then wonder why their "optimized" approach stops working. The answer is noise. Small samples fit random variance, not repeatable edge.

At least 20 trades per filtered segment are required for moderate statistical reliability. Below 10 trades per cell, you are fitting noise rather than signal. That threshold applies to every filter layer you add, not just the top-level setup category.

Here is where traders go wrong most often:

- Splitting a 40-trade breakout sample into four session-time buckets leaves 10 trades per cell. That is noise territory.

- Adding a third filter (say, VIX level) to an already-thin sample destroys statistical meaning entirely.

- Declaring a setup "fixed" after two good weeks ignores the sample size requirement completely.

A setup must be tested against 20 to 30 or more filtered occurrences per category to be statistically meaningful. Aggregate win rates often mask regime-specific underperformance, which is why granular, sufficiently sized subgroups are non-negotiable.

The practical fix is to limit your filter layers. Two filters maximum per analysis pass. If your sample shrinks below 20 trades in any cell, collapse that filter until you collect more data. Pre-declare your categories before analyzing, not after. Post-hoc category creation is the fastest route to overfitting and a strategy that fails in live markets.

How many confluence factors actually improve a setup?

More indicators do not mean better signals. This is one of the most expensive misconceptions in retail trading. Stacking five or more confluence factors collapses your sample size, increases decision latency, and produces analysis paralysis rather than cleaner entries.

Optimal confluence for retail traders is 2 to 4 independent factors. Beyond that threshold, sample size drops and decision latency harms performance. The three-factor framework, one momentum signal, one volume confirmation, one price action context, provides the best balance between signal quality and trade frequency.

| Factor count | Signal quality | Trade frequency | Risk |

|---|---|---|---|

| 1 factor | Low | Very high | Too many false signals |

| 2 to 3 factors | High | Moderate | Optimal for most styles |

| 4 factors | Moderate | Lower | Manageable if factors are independent |

| 5 or more factors | Diminishing | Very low | Sample collapse and paralysis |

Factor independence is the key variable most traders ignore. Two momentum indicators (RSI and Stochastic, for example) are not two independent factors. They measure the same underlying condition and add near-zero incremental information. A professional breakout setup, by contrast, might combine a price structure trigger, volume at 1.5 times the 20-day average to confirm institutional participation, and a higher-timeframe trend context. Those three factors come from genuinely different data categories.

Run a quarterly audit of your confluence stack. Remove any factor that correlates above 0.7 with another factor already in your setup. Pruning redundant indicators quarterly preserves independence and prevents the slow creep of confluence inflation that causes traders to miss entries or second-guess valid signals.

Pro Tip: If you trade lower timeframes on crypto or forex, cap your confluence at three factors. Higher-frequency setups require faster decisions, and a fourth factor often costs you the entry entirely.

How does multi-strategy routing improve trading performance?

No single strategy works best across all market conditions. A breakout strategy that thrives in a trending market bleeds in a range. A mean-reversion approach that excels in low-volatility chop gets destroyed in a momentum spike. The fix is regime detection paired with a strategy router that assigns the right approach to the current market state.

A strategy router that selects the best strategy per market regime yields better long-term returns than any universal approach. A concrete example: Bollinger Band squeeze strategies jump from 56 percent to over 80 percent accuracy when filtered by proper regime conditions. That is not a small improvement. It is the difference between a marginal edge and a strong one.

Here is how to build a basic routing framework:

- Trending markets: Use breakout and momentum continuation setups. Avoid mean-reversion entries.

- Ranging markets: Use range fade and support/resistance bounce setups. Avoid breakout entries.

- High-volatility events: Reduce position size by 50 percent or sit out entirely. Volatility gating prevents outsized losses.

- Regime detection tools: Average Directional Index (ADX) above 25 signals trend. ADX below 20 signals range. You can also use volatility as a filtering factor to gate entries.

Multi-instrument application compounds this further. Applying the same strategy rules across 3 to 5 different market instruments can double or quadruple the strategy's practical value without changing any parameters. This is often faster and more effective than tweaking entry rules. Applying a proven futures strategy to correlated instruments, for example, is a direct way to expand strategy value without rebuilding from scratch.

Use Walk-Forward Optimization (WFO) to validate your routing logic. WFO tests your strategy on out-of-sample data in rolling windows, which prevents the overfitting that destroys backtested results in live markets. Tie position sizing directly to WFO confidence levels. High-confidence validated setups get full size. Setups in validation get half size.

Key takeaways

Optimizing trading setups requires clean data tagging, statistically valid sample sizes, independent confluence factors, and regime-aware strategy routing to produce durable, measurable performance gains.

| Point | Details |

|---|---|

| Tag every trade at entry | Assign a setup label and confidence rating to unlock meaningful performance analysis. |

| Filter by profit factor | Cut any setup with a profit factor below 1.0 across 20 or more trades to improve monthly P/L. |

| Require 20 trades per segment | Any filtered cell below 20 trades is statistical noise, not a repeatable edge. |

| Use 2 to 4 independent factors | Independent confluence factors from different signal categories outperform stacked redundant indicators. |

| Route strategies by market regime | Matching the right strategy to the current market state significantly increases win rate and overall returns. |

What I've learned from years of setup optimization

The single biggest mistake I see retail traders make is optimizing for complexity instead of clarity. They add a fourth indicator, then a fifth, then wonder why their live results look nothing like their backtest. The answer is almost always sample size collapse combined with correlated factors that felt independent but were not.

Strict tagging discipline changed everything for me. Tagging FOMO trades honestly is uncomfortable. You see exactly how much those impulsive entries cost. But that discomfort is the data telling you something real. Ignore it and you optimize around a fiction.

Multi-instrument application is underrated. Running a validated setup across Bitcoin, EUR/USD, and ES futures simultaneously gave me three times the trade frequency without touching the entry rules. The fastest improvement often comes from deploying what already works in more places, not from rebuilding what is broken.

My honest caution: monthly reviews feel tedious until the month you catch a setup that quietly turned negative. That one catch pays for every review you ever do. Build it into your calendar like a bill payment. It is not optional if you want consistent performance.

— Tran

How Scalping-algo's tools put these techniques into practice

Scalping-algo builds its premium TradingView indicators specifically for the kind of regime-aware, confluence-filtered trading this article describes. Every indicator is built in Pine Script v6, generates non-repainting signals, and includes volatility gating so you are not entering setups in conditions that historically destroy them.

The Algo Master 3-indicator suite applies exactly the 2 to 4 independent factor framework covered above: momentum, volume confirmation, and price action context working together without redundancy. It is designed for crypto, forex, indices, and futures on the 1-minute to 15-minute timeframes where regime detection and fast execution matter most. The Command Center dashboard ties alerts, backtesting, and performance tracking into one place, so your setup review process takes minutes instead of hours.

FAQ

What is the most important metric for filtering trading setups?

Profit factor is the primary metric for setup filtering. A profit factor above 1.3 over 30 or more trades signals a meaningful edge, while any setup below 1.0 with sufficient sample size should be cut.

How many trades do I need before a setup result is reliable?

You need at least 20 trades per filtered segment for moderate statistical reliability. Below 10 trades, results reflect random variance rather than a repeatable edge.

How many confluence factors should a trading setup have?

Two to four independent factors is the optimal range. Stacking five or more factors collapses sample size and increases decision latency without improving signal quality.

What is a strategy router in trading?

A strategy router assigns the best-fit strategy to the current market regime, such as breakout strategies for trending markets and mean-reversion approaches for ranging conditions. This regime-matching approach can push win rates significantly higher than using a single universal strategy.

How do I avoid overfitting when refining my trading setups?

Pre-declare your setup categories before analyzing data, limit filter layers to two per analysis pass, and validate results using Walk-Forward Optimization on out-of-sample data. Post-hoc category creation is the primary cause of overfitting in retail trading analysis.