Most traders set their parameters once and forget them. They pick a stop-loss, a position size, and an entry threshold, then run the same settings through bull markets, bear markets, and everything in between. That approach quietly bleeds performance. This adaptive trading parameters guide breaks down exactly why static settings fail, what adaptive parameters actually are, and how you implement them without over-engineering your strategy. Whether you trade crypto, forex, or futures on lower timeframes, what follows is the practical framework you need to stay calibrated as markets shift.

Table of Contents

- Key Takeaways

- Understanding adaptive trading parameters

- How adaptive adjustment mechanisms work

- Best practices for implementation

- Common pitfalls and how to avoid them

- Adaptive parameters in action: scenario examples

- My honest take on adaptive parameter strategies

- Take your parameters further with Scalping-Algo

- FAQ

Key Takeaways

| Point | Details |

|---|---|

| Static parameters eventually fail | Fixed settings cannot account for changing market regimes, volatility spikes, or shifting momentum. |

| Adaptation needs a risk framework | Dynamic adjustment only works when hard risk caps and baseline rules govern how far parameters can move. |

| Run a control strategy in parallel | Compare your adaptive system against a static version to confirm adaptation is generating real performance gains. |

| Dampening prevents self-whipsaw | Use rolling averages and minimum change thresholds to stop frequent noise-driven updates from degrading results. |

| Walk-forward testing is non-negotiable | Validate adaptive parameters across multiple market regimes before going live. |

Understanding adaptive trading parameters

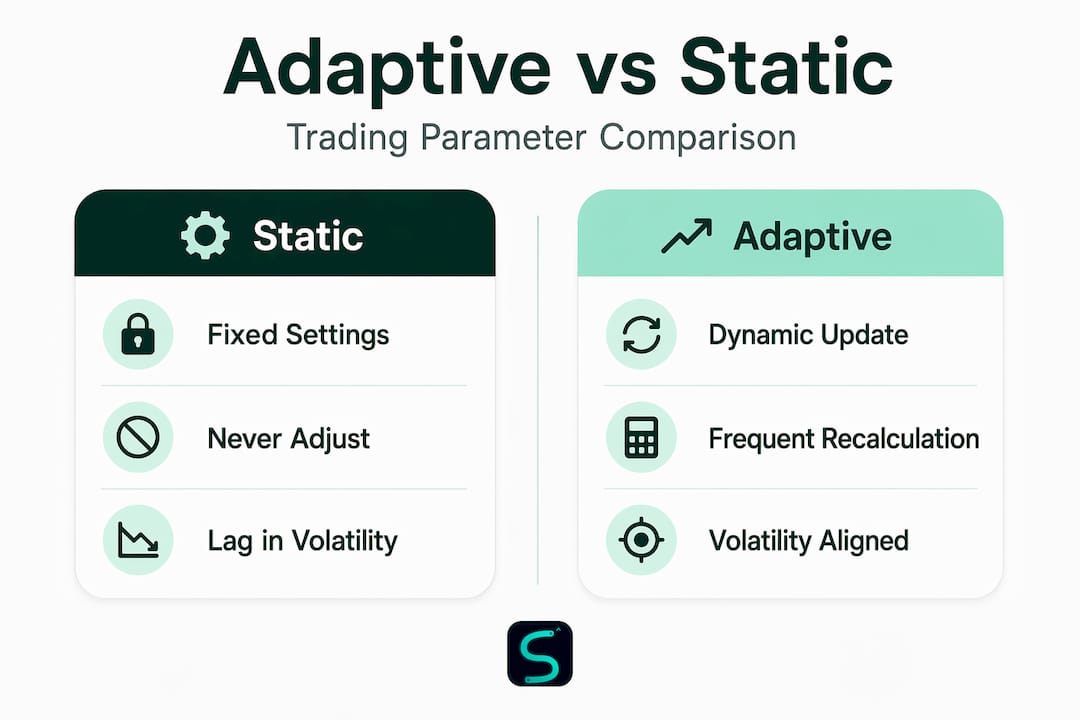

At its core, an adaptive trading parameter is any variable in your strategy that updates based on live market feedback rather than staying fixed at an initial value. This is the fundamental distinction. Static parameters are set once. Adaptive parameters are re-evaluated continuously.

The most common adaptive parameters in practice include:

- Position sizing. Adaptive frameworks adjust trade size dynamically based on current volatility, drawdown levels, and account status. Size shrinks during volatility spikes to protect capital and expands during calm, trending conditions to capture more edge.

- Stop-loss levels. Rather than a fixed pip or percentage stop, an adaptive stop moves with the current Average True Range or volatility reading. A quiet EUR/USD session and a post-NFP spike deserve different stop distances.

- Entry and exit thresholds. Momentum signals, divergence triggers, and breakout confirmation levels that shift based on recent price behavior rather than fixed values set during backtesting.

- Order timing and price limits. Adaptive algorithms adjust order size, timing, and price limits based on real-time execution performance and market conditions, balancing capital exposure with volatility constraints.

Here is how adaptive compares to static approaches at a glance:

| Feature | Static Parameters | Adaptive Parameters |

|---|---|---|

| Adjustment frequency | Never (set once) | Continuously or on regime change |

| Market regime awareness | None | Built into logic |

| Overfitting risk | Moderate | Higher if not managed carefully |

| Capital protection | Rigid, may expose too much | Scales with current risk environment |

| Implementation complexity | Low | Moderate to high |

The goal of trading parameter optimization is not to chase every market move. It is to keep your strategy's risk and reward settings calibrated to what the market is actually doing right now.

How adaptive adjustment mechanisms work

Understanding the mechanics helps you build or evaluate any adaptive framework with confidence. This is where theory meets execution.

-

Real-time data feeds. Every adaptive system starts with live market data. Volatility measures like ATR, volume profiles, and order flow metrics feed the adjustment logic. Without clean, low-latency data, the system reacts to stale signals.

-

Regime detection. Parameter adjustments tied to regime awareness produce better risk-adjusted outcomes. Trending, ranging, and volatility-burst regimes each require different parameter settings. A regime detector identifies the current state and routes the strategy to appropriate parameter sets.

-

Continuous model ranking. Adaptive systems re-evaluate model rankings based on rolling recent market data rather than relying on historical performance from months ago. The model that worked best last week may not be the best fit today. Continuous evaluation catches that drift early.

-

Algorithmic and genetic optimization. Genetic algorithms can run thousands of parameter combinations against recent data to find configurations that score well on stability and performance simultaneously. This is not manual parameter tweaking. It is systematic search.

-

Frictionless live adjustment. Modern infrastructure supports real-time parameter tuning without stopping or recreating a running strategy. This is critical for scalpers on 1-minute to 5-minute charts who cannot afford strategy downtime during active sessions. Understanding how algorithmic trading benefits scalpers starts with this kind of infrastructure flexibility.

-

Dampening factors. This is the step most traders skip and then regret. Applying dampening factors like rolling averages or minimum change thresholds prevents the system from reacting to short-term noise. Without dampening, you get parameter oscillation. With it, updates are smooth and deliberate.

Pro Tip: Set a minimum change threshold for each adaptive parameter. If a new volatility reading suggests moving your stop from 12 pips to 13 pips, that update may not be worth the added transaction cost and complexity. Only trigger updates when the signal crosses a meaningful threshold.

Best practices for implementation

Getting adaptive parameters right in live trading comes down to structure and discipline. Here is what actually works.

- Define hard risk caps first. Before any parameter updates, set absolute limits. Maximum position size as a percentage of account, maximum daily drawdown before trading pauses, and minimum stop-loss distance are non-negotiable floors. Adaptation should enforce risk controls, not bypass them.

- Set evaluation windows carefully. A 5-bar lookback window responds too quickly to noise. A 200-bar window responds too slowly to be useful on a 5-minute chart. Match your evaluation window to your timeframe. For scalping on 1m to 15m charts, a 20 to 50 bar rolling window often provides the right balance.

- Run a static control in parallel. A control strategy ensures adaptive benefits are genuine and not caused by increased complexity or hidden transaction costs. If your adaptive version is not outperforming the static version on a risk-adjusted basis after 200 or more trades, the adaptation is adding noise, not alpha.

- Run walk-forward validation. Backtesting alone is not enough. Walk-forward testing splits your historical data into training and testing windows and rolls them forward chronologically. This reveals whether parameter adjustments hold up across different market regimes or only look good on the training period.

- Score for robustness, not just return. A parameter set that earns 30% returns with 45% drawdown is not better than one earning 18% with 12% drawdown. Build stability scoring into your evaluation. Metrics like the Calmar ratio and win-rate consistency across regimes matter more than peak returns.

Pro Tip: Avoid the trap of constant re-optimization. Run your adaptive evaluation on a scheduled basis, weekly or daily depending on your timeframe, rather than tick by tick. Tick-level re-optimization creates curve-fitting risk and inflates transaction costs.

The role of volatility in scalping is especially relevant here. Volatility is both the trigger for parameter updates and the biggest risk factor when those updates misfire.

Common pitfalls and how to avoid them

Even experienced traders stumble on the same set of problems when deploying adaptive strategies. Knowing these upfront saves weeks of frustration.

-

Parameter oscillation. Too-frequent updates based on short-term noise cause the system to whipsaw itself. Your stop-loss widens then tightens then widens again within the same session. The fix is dampening: rolling averages, minimum change thresholds, or update-frequency limits.

-

Overfitting to recent data. Adaptive systems that re-optimize too aggressively on recent performance will appear brilliant in backtests and struggle in live markets. The system learns the recent noise rather than the underlying market structure. Walk-forward testing and out-of-sample validation are the primary defenses.

-

Complexity without proportional benefit. Every layer of adaptation adds development time, monitoring overhead, and potential failure points. If adding regime detection improves your Sharpe ratio by 0.1, ask whether that improvement justifies the added complexity. Efficient trading techniques prioritize measurable improvement over theoretical elegance.

-

Ignoring transaction costs. Adaptive sizing and frequent threshold adjustments can increase your average trade count. On tighter spreads in liquid markets, this is manageable. On wider spread instruments or at lower account sizes, the friction adds up faster than the adaptation earns.

-

Abandoning risk discipline during adaptation. Some traders interpret dynamic adjustment as permission to let the system override their risk rules. It is not. Structured frameworks with risk-preserving controls enhance adaptive logic. Removing those controls invites the kind of drawdowns that end accounts.

Adaptive parameters in action: scenario examples

Theory is useful. Seeing it applied is more useful. Here are two concrete scenarios showing how adaptive parameters shift real trading outcomes.

Scenario 1: Volatility-based adaptive position sizing during a news event. A crypto scalper is running a BTC/USDT strategy on the 5-minute chart. ATR spikes 3x above its 20-bar average following a Federal Reserve statement. The adaptive sizing logic detects this regime shift and halves position size immediately. The subsequent 400-point whipsaw hits the stop, but the reduced size limits the loss to 0.4% of account rather than the 0.9% a static system would have taken. Capital protection in real time, no manual intervention needed.

Scenario 2: Regime-aware model ranking improving entry timing. A forex scalper uses a multi-model ranking system on EUR/USD. On a trending day, the system ranks momentum-based entry signals highest. On a ranging day, it ranks mean-reversion signals highest. Continuous model re-evaluation based on rolling data shifts signal weighting dynamically. Over 100 trades, win rate on trending days improves by 8 percentage points compared to a static signal-weighting approach.

| Scenario | Static Result | Adaptive Result |

|---|---|---|

| News-driven volatility spike | 0.9% account loss | 0.4% account loss |

| Trending vs. ranging day signals | Fixed win rate | +8% win rate on trend days |

| Grid parameter update during session | Requires strategy restart | Live update, zero downtime |

These numbers are scenario-based illustrations, not guaranteed outcomes. But they represent the kind of directional improvement adaptive frameworks consistently produce when implemented correctly.

My honest take on adaptive parameter strategies

I've watched traders treat adaptive parameters like a silver bullet. Build the logic, turn it on, and let it run. That mindset is the fastest way to blow up a system that looked great in testing.

What I've learned from working with adaptive frameworks across multiple asset classes is this: the adaptation itself is almost never the hard part. The hard part is the risk architecture underneath it. If your baseline rules are weak, dynamic adjustment amplifies the weakness. If your position sizing caps are too loose, adaptive sizing will eventually push you into oversized trades during a deceptively calm regime just before a volatility spike.

The insight most traders miss is that running a static strategy alongside your adaptive one is not optional. It is how you know whether your adaptation is actually working. I've seen adaptive systems with impressive backtests that underperformed their static counterparts in live trading for three months straight. Without the control, you would never catch that.

My practical advice: start simple. One adaptive parameter. Volatility-adjusted sizing is the best place to begin because the logic is transparent and the benefit is measurable. Add regime detection only after you have stable results with sizing adaptation alone. Avoid building a system so complex that you cannot explain why it is making a specific decision on any given trade. Complexity you cannot explain is complexity you cannot defend when the drawdown arrives.

— Tran

Take your parameters further with Scalping-Algo

If you want to apply what you have learned without building everything from scratch, Scalping-Algo's tools are built exactly for this.

Scalping-Algo's premium TradingView indicators are built in Pine Script v6 with adaptive logic baked in: volatility gating, divergence detection, and confluence filtering that adjusts to real-time market conditions across crypto, forex, indices, and futures. The Algo Master suite specifically demonstrates how three coordinated indicators work together to implement flexible parameter strategies without manual re-tuning between sessions. Every script is open-source and non-repainting. For traders who want full transparency on how performance is measured, the evaluation methodology page covers exactly how Scalping-Algo validates its signals across market regimes. This is the kind of infrastructure that makes adaptive trading parameters practical, not just theoretical.

FAQ

What are adaptive trading parameters?

Adaptive trading parameters are strategy variables like position size, stop-loss levels, and entry thresholds that automatically update based on live market feedback rather than remaining fixed. They allow a strategy to stay calibrated to current market conditions rather than relying on settings optimized for past conditions.

How do you prevent parameter oscillation in adaptive systems?

Apply dampening factors such as rolling averages or minimum change thresholds to your parameter update logic. These filters prevent the system from reacting to short-term noise and triggering constant, counterproductive adjustments.

Why run a static strategy alongside an adaptive one?

Running a static control strategy lets you objectively measure whether your adaptive system is generating genuine performance improvements or simply adding complexity and transaction costs. Without a control, you cannot isolate the true contribution of your adaptive logic.

What is the best first parameter to make adaptive?

Position sizing based on current volatility is the best starting point. The logic is transparent, the benefit is measurable, and the implementation is straightforward compared to full regime-detection systems. Start with volatility-adjusted sizing before adding more complex adaptive layers.

How often should adaptive parameters update?

Update frequency should match your trading timeframe. For scalping on 1-minute to 15-minute charts, a rolling window of 20 to 50 bars strikes the right balance between responsiveness and stability. Tick-level re-optimization creates overfitting risk and inflates transaction costs unnecessarily.